Catching Up and Falling Behind: Economic Convergence in Europe

EMBARGO

Not to be released before

Wednesday, 3 May 2000

00:01 GMT

Press Release

ECE/GEN/00/14

Geneva, 26 April 2000

UN/ECE releases its first 2000

Economic Survey of Europe

Are the standards

of living of west Europeans catching up with those of north Americans? Are the standards

of living of the inhabitants of countries with economies in transition reaching west

European levels? Is there any convergence between all these countries in terms of per

capita GDP? Those are some among the many questions which are answered in chapter 5 of the

latest release of the Economic Survey of Europe 2000, No. 1 just published by

the United Nations Economic Commission for Europe (UN/ECE).

"The issue of convergence is not only

important in the context of west European economic and monetary integration",

stresses Paul Rayment, Director of the Economic Analysis Division of the UN/ECE, "but

also for the wider European integration process. One of the strategic goals of the

transition economies is to achieve sustained and high rates of economic growth that would

enable them to catch up with – to converge upon – the living standards of the

developed economies of western Europe. And many of them regard EU membership as

instrumental to promote this process."

Western Europe and North America - the

widening gap

"Since the early 1950s"

comments Dieter Hesse, a senior economist and head of the market economies section of the

UN/ECE, "there has been a long-run tendency for the inequality of real per capita GDP

across developed market economies of the region to decline over time. This so-called

"sigma convergence", however, was most pronounced during the period 1950-1973,

also known as the Golden Age of post-war economic growth. In contrast, there was a marked

slowdown in convergence in the post-1973 period." The progress in convergence in the

period 1950-1998 reflects a tendency for countries with below average per capita GDP in

the initial period to experience a faster rate of growth thereafter. The speed of

convergence is, however, very slow.

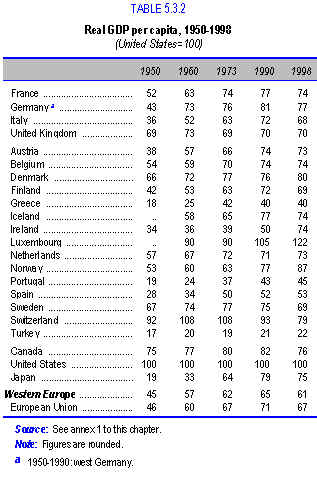

Using the per capita GDP of the United

States as a benchmark, the feature in western Europe was for strong convergence on the

United States’ real GDP per capita in the period 1950-1973, but this catch-up process

then slowed down markedly. "On average, there was little further progress in closing

the real income gap relative to the United States after 1973; in fact, the gap widened

slightly in the 1990s" stresses Dieter Hesse. Thus, despite considerable

progress since 1950, there remains a large difference between real per capita GDP in the

United States and in western Europe: the gap amounted to some 40 per cent for the

aggregate of 19 west European countries and some 33 per cent for the EU in 1998 (see

table 5.3.2).

The available evidence suggests that the

process of convergence to US per capita income levels (and also convergence within western

Europe) reflects to a large extent productivity catch-up and technical change. The notable

weakening of the tendency for convergence in western Europe after 1973 may be due to the

adverse impact of successive shocks on macroeconomic stability and longer-term growth

expectations. These, in turn, reduced the stimulus to fixed investment, which is the main

vehicle for technical change. Greater cyclical volatility can also influence the longer

term growth performance via its impact on "learning by doing" and,

therefore, on human capital formation, both of which may slow down in periods of low

growth or recession.

Progress in convergence has been uneven

across countries (notably at the European periphery) and over time, reflecting the

specific interactions between domestic and international factors and their impact on the

growth of individual countries. This suggests that the longer term growth performance of

each country is essentially unique, and therefore difficult to replicate. Ireland is a

prime example of convergence: its real per capita GDP rose from some 60 per cent of the EU

average in 1960 to 110 per cent in 1998. But the Irish success has been the result of the

favourable interaction of a host of specific factors (such as conducive changes in the

western European and global economic environment and a skilful policy designed to attract

foreign direct investments (FDI)) which is unlikely to be repeated elsewhere. Convergence

petered out into broad stagnation in Greece after 1973 and catch-up never really took off

in Turkey. In contrast, the performance in Portugal and Spain has been more pronounced,

although whether the outcome could have been even better remains an open question. The

more favourable outcome for Portugal and Spain compared with Greece after 1973 has been

associated inter alia with a greater emphasis on institutional adaptation,

macroeconomic stabilization, structural reforms and trade liberalization in the former two

countries, which together created a more conducive environment for foreign direct

investments (FDI).

The empirical evidence also emphasises the

inter-relatedness of short-term cyclical developments and longer term economic growth. In

fact, the growth performance of this group of developed market economies was rather uneven

over the period 1950-1998, with episodes of weaker growth followed by more or less long

periods of sustained dynamism (or vice versa). This points to the role of

country-specific characteristics, including (positive or adverse) shocks and policies in

determining long-term growth patterns apart from common factors such as technological

change. Thus, adverse cyclical conditions and arduous structural adjustments led to the

virtual stagnation of real per capita GDP in Sweden and even a small decline in

Switzerland in the 1990s.

Eastern Europe and the CIS: Divergence during the

Transition

"Despite all the methodological

difficulties and data problems, over the long run (during the 50-year period between 1950

and 2000), it is clear that there is little evidence of catching up by the former

centrally planned economy countries (CPEs) and their successor states on the per capita

income levels of the EU-15", says Rumen Dobrinsky, a senior economist in the

transition economies section of the UN/ECE. On the contrary, a comparison of per capita

GDP in the initial and final years reveals instead evidence of falling behind; the latter

is especially pronounced in the successor states of the Soviet Union after 1990. The only

evidence, which was found, of absolute convergence in per capita income levels within the

former CPEs as a group and in relation to some of the west European economies was during

the 1950s and 1960s. Starting from the 1970s the gaps in income levels started to widen

again.

"One striking result of our study is

that the eastern part of the continent was already characterized by high and increasing

economic heterogeneity by the end of the 1980s. This finding is at odds with the

widespread view that central planning and economic cooperation within the CMEA had

instigated a relatively high level of economic homogeneity and a leveling of per capita

income levels within the group", adds Rumen Dobrinsky. In fact, the Survey shows that the general slowing down of economic growth in the 1970s was followed by a

rapid divergence during the 1980s.

The start of economic and political

transformation after 1989 generated high hopes and expectations on the part of the peoples

living in the eastern part of the continent of fast improvement in their living standards

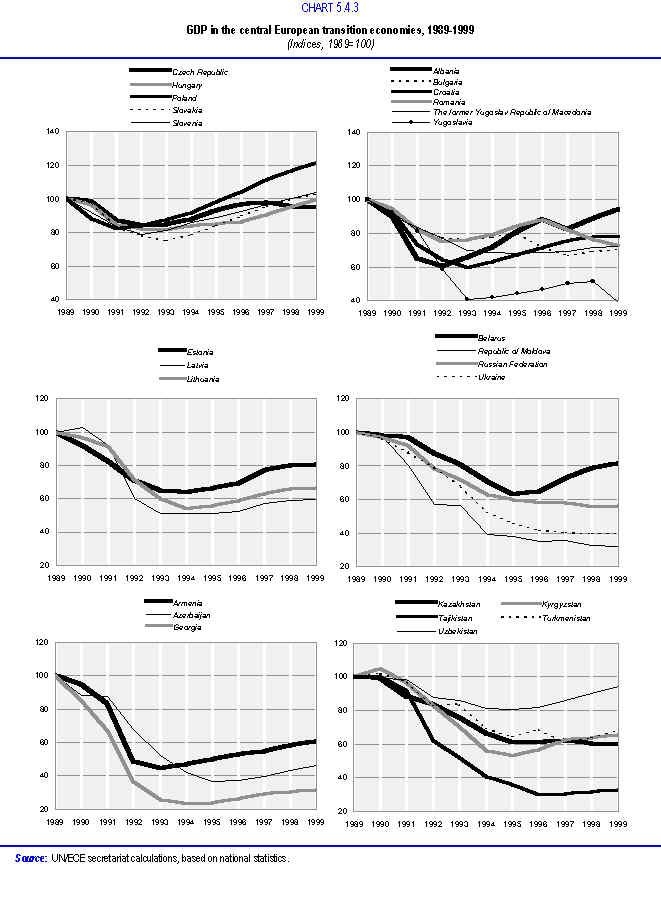

and of catching up with those prevailing in western Europe. However, the past decade has

been characterized by highly divergent paths of growth among the transition economies:

while some of them have embarked on a path of sustained recovery, others are still

struggling with the transformational recession (see chart 5.4.3). By 1999 the central

European transition economies had either regained (Poland, Slovakia, Slovenia) or were

close to their pre-transition GDP levels (Czech Republic, Hungary); at the same time in

countries such as Georgia, the Republic of Moldova, Ukraine and Yugoslavia, GDP in 1999

was a mere one third of its pre-transition level.

In 1999 the average per capita GDP level

(measured using purchasing power parities (PPP)) in the five central European transition

economies was 46 per cent of the average per capita GDP level in the EU-15, and this

proportion was almost unchanged from a decade ago, while in the seven south-east European

transition economies average per capita income had fallen to 22 per cent of the EU-15

average from 39 per cent in 1989. In the three Baltic states the average per capita GDP in

1999 was 31 per cent of the EU-15 average while for the CIS countries as a whole this

number was 24 per cent.

In general, the transition to a market

economy has brought about turbulent changes and growing evidence of economic heterogeneity

and divergence in per capita income levels in the former CPEs. At the same time there

emerged subgroups of transition economies in which per capita incomes were more

homogeneous. Some of them (notably central Europe during the second half of the 1990s)

were also beginning to catch up on west European levels, but most of the transition

economies continued to diverge from one another and to fall further behind the income

levels of western Europe.

"Convergence in Europe, namely, the

process closing of per capita income gaps between the transition economies and western

Europe, is likely to be long and difficult" stresses Rumen Dobrinsky. "The

time required for catching up can be estimated in decades, even for the more advanced

transition economies and under optimistic growth scenarios". The main prerequisite

for convergence in Europe is a rapid and sustained rate of growth of the transition

economies. Although their past experience may not be very encouraging, the start of

economic transformation has created an opportunity for breaking with the past and for

establishing a favourable environment for growth and catching up.

Several proximate factors are however

necessary for achieving high and sustained long-term economic growth. These are:

investment in physical and human capital; investment in research and development and

infrastructural development; openness to trade; the development and upgrading of financial

systems; and maintaining a generally acceptable distribution of wealth within each

country; as well as a range of institutional, social and political factors.

For further information please contact:

Economic Analysis Division

United Nations Economic Commission for Europe (UN/ECE)

Palais des Nations

CH - 1211 Geneva 10, Switzerland

Tel: (+41 22) 917 27 78

Fax: (+41 22) 917 03 09

E-mail: [email protected]

Website: http://www.unece.org/ead/ead_h.htm

|

In order to provide you

with a better service, we would appreciate it if you would send a copy of your

article to: Information Unit, United

Nations Economic Commission for Europe (UN/ECE), Palais des Nations, Room 356, CH - 1211

Geneva 10, Switzerland,

Tel: +(41 22) 917 44 44, Fax: +(41 22) 917

05 05,

E-mail: [email protected],

Website: http://www.unece.org

Thank you. |