External conditions, policy uncertainty and structural changes are weighing on growth momentum

Growth in Europe is projected to remain moderate, as the region continues to face multiple downside risks, according to the United Nations World Economic Situation and Prospects (WESP) 2020, which was launched today.

The Report states that the global economy suffered its lowest growth in a decade, slipping to 2.3 per cent in 2019, as economic activity was impacted by prolonged trade disputes. The world, however, could see a slight uptick in growth in 2020 if risks are kept at bay.

While global growth of 2.5 per cent in 2020 is possible, the Report cautions that a flareup of trade tensions, financial turmoil, or an escalation of geopolitical tensions could derail a recovery. In a downside scenario, global growth would slow to just 1.8 per cent this year. A prolonged weakness in global economic activity may cause significant setbacks for sustainable development, including the goals to eradicate poverty and create decent jobs for all. At the same time, pervasive inequalities and the deepening climate crisis are fuelling growing discontent in many parts of the world.

UN Secretary-General António Guterres warned that “These risks could inflict severe and long-lasting damage on development prospects. They also threaten to encourage a further rise in inward-looking policies, at a point when global cooperation is paramount.”

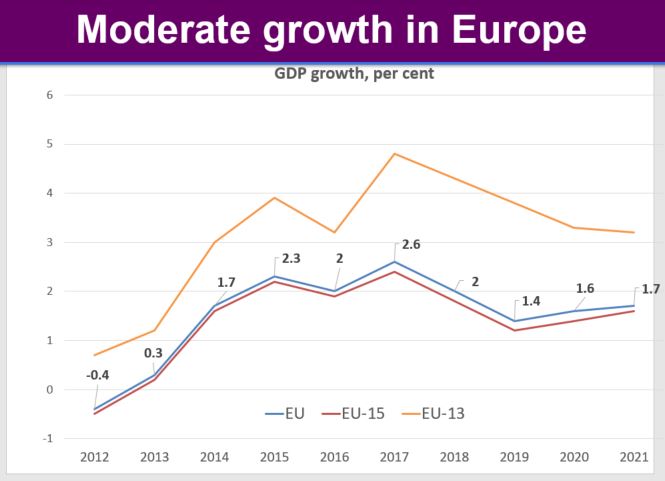

Europe is expected to see only limited growth of 1.6 per cent in 2020 and 1.7 per cent in 2021. Against the backdrop of heightened global trade tensions, exporters face numerous challenges, including tariffs, weaker demand, and greater policy uncertainty. In addition, structural challenges and changes in significant sectors, such as the car industry put long-established business models in doubt and create the need for companies and policymakers to develop new economic paradigms. As these factors will weigh on the contribution of exports to economic performance, domestic demand will remain the mainstay of growth. Lower unemployment, solid wage gains and additional stimulus on top of the already supportive monetary stance will underpin robust household consumption. The very accommodative monetary policy stance will continue to drive investment in domestically oriented sectors such as residential construction, creating positive knock-on effects for many small and medium-sized companies.

The members of the EU from the Baltics, Central and Eastern Europe, and the Western Balkans that joined the Union since 2004 (EU-11) are expected to register GDP growth rates well above the European Union average in 2020-2021. In several of those countries, growth likely exceeded 4 per cent in 2019, facilitating their gradual convergence towards the more advanced economies of the European Union. Unemployment rates in the EU-11 have dropped to record lows and real wages have soared, stimulating private consumption. Export performance of the Eastern European industrial sector remained one of the growth drivers. However, the external environment for those countries is becoming more challenging. Structural challenges in the automotive industry will weigh on production and exports, and EU financing from the 2021-2027 Multiannual Financial Framework of the European Union is expected to be lower. Stronger inflationary pressures may also lead to some policy tightening.

Risks and policy challenges

The outlook for Europe remains subject to numerous risks and challenges that could lead to a significant slowdown in growth. First, an escalation of trade tensions could have a considerable impact on European exporters, affecting not only direct exports but also exports from foreign production sites—including, for example, various models produced by European car manufacturers in the United States for export to China.

Second, the exit of the United Kingdom from the European Union remains an unresolved issue. While the baseline forecast assumes that the United Kingdom will leave the European Union with a formal agreement, a disorderly exit with no agreement would open the field to a host of negative consequences across the real economy and financial markets. With the modalities of the exit unclear and no indications as to the nature and structure of the legal and economic relations of the United Kingdom with the European Union and the rest of the world after the exit, corporate investment decisions are already facing tremendous policy uncertainty.

A third risk stems from monetary policy. After a brief period of starting to move away from a very accommodative policy stance, the European Central Bank has again reversed course by providing even more stimulus, in response to persistently low inflation and global economic challenges. This will increase the potential for a run-up in asset prices, with associated risks to financial stability. It also leaves little scope for additional monetary easing in the event of an economic crisis.

For more information, please visit: www.bit.ly/wespreport